On March 1, 2026, the global macro markets encountered an epic "black swan" event: direct military strikes by the United States and Israel against Iran resulted in the death of Iran's Supreme Leader, Ayatollah Khamenei.

This extreme tail-risk event instantly reshaped the risk premium models for global asset classes. The complete ignition of the Middle East powder keg not only caused violent fluctuations in traditional crude oil and safe-haven assets but also pushed the cryptocurrency market, at a critical juncture of博弈, to a crossroads of liquidity and pricing power.

Combining Binance spot market data with Deribit option data, this analysis delves into the immediate impact of this geopolitical crisis on the cryptocurrency market from a quantitative and derivatives博弈 perspective, offering a forward-looking projection of future volatility paths and market trends.

The essence of geopolitical conflict is the reshaping of global supply chains, energy prices, and the ensuing inflation expectations. The financial market transmission of this surprise US-Israel attack on Iran manifested as a textbook risk-aversion pattern: commodities like crude oil and gold became the preferred safe havens, while high-risk assets faced indiscriminate selling in the first instance.

With the outbreak of high-intensity conflict in the Middle East, the primary concerns are the global energy supply chain and the safe-haven sentiment towards the fiat currency credit system. In traditional financial markets, Brent crude oil is highly likely to gap up on open due to panic over potential supply disruptions, and traditional safe-haven assets like gold will also see intensive accumulation by institutional funds. However, in the crypto asset space, BTC's "digital gold" narrative and its "high-beta risk asset"属性 are experiencing intense internal conflict.

From a macro liquidity perspective, panic induced by geopolitics (a soaring VIX index) typically triggers cross-asset indiscriminate selling in the first instance to secure US dollar liquidity. But after a brief liquidity squeeze, Bitcoin, which is不受特定主权国家控制 and possesses抗审查与便携属性, often attracts capital fleeing from high-risk emerging market fiat currencies.

Combining Binance's spot and contract market data (as of 14:00 on March 1, 2026), the BTC/USDT spot price is oscillating around $67,392. In the initial phase of such a major geopolitical crisis, BTC did not experience a crash similar to the "312" event of 2020 but tenaciously held the key support level of $67,000.

The 24-hour trading volume reached a high of $1.74 billion, indicating significant disagreement and turnover between bulls and bears at this level. The moving average system in the price chart shows a pattern of high volatility after a多头排列, suggesting that, under the impact of sudden news, the承接盘力量 in the spot market is exceptionally robust, and the long-term配置底仓 of institutional funds has not fundamentally shifted.

To透视聪明资金的真实意图, the derivatives market, especially option data, provides the most直观的量化截面. By analyzing the current BTC option data expiring on March 27, 2026, on the Deribit platform, we can clearly outline the path projection of major institutions for the next month.

The current implied volatility (IV) for BTC options expiring on March 27 has reached a relatively high level of 51.3%. Against the backdrop of the geopolitical crisis, option sellers quickly raised the volatility surface to hedge against the Gamma exposure risks posed by extreme market movements. An IV above 51% indicates the market is hedging against potential wide fluctuations in the next two to three weeks. For quantitative traders, the risk-reward ratio for selling volatility at this time is extremely poor, and the market is overall in a frenzy of "buying straddles" or constructing tail-risk protection.

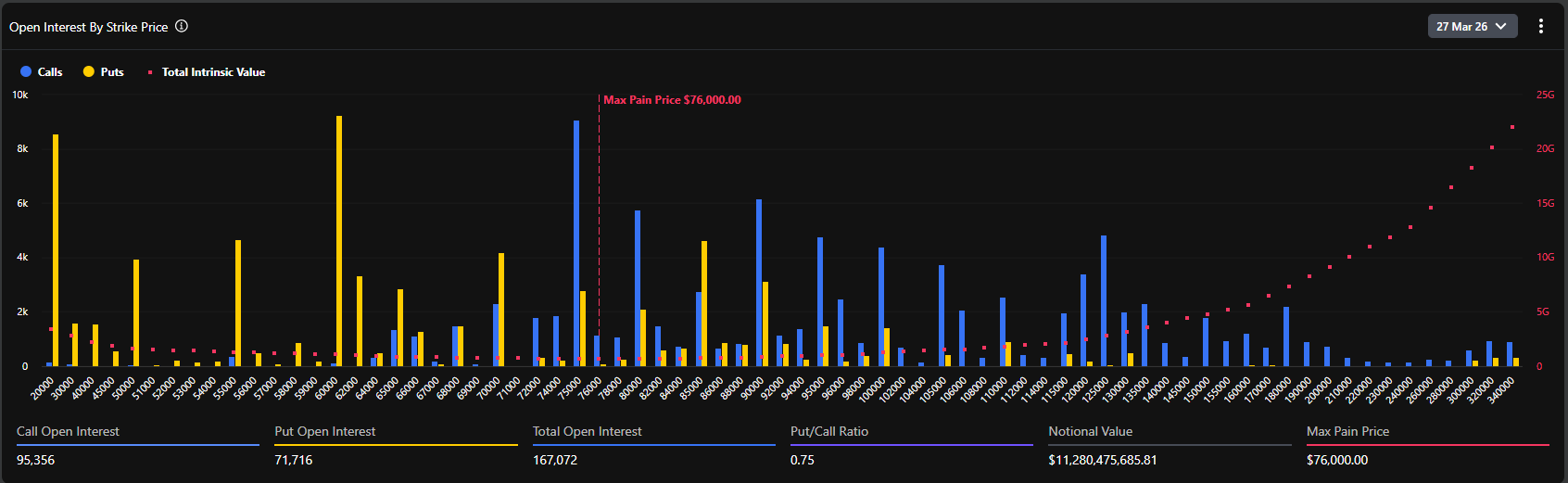

According to the open interest (OI) distribution chart for options, the current global maximum pain point is as high as $76,000. This is a highly forward-looking and controversial data point.

Typically, as expiration approaches, the underlying asset price tends to gravitate towards the maximum pain point to minimize the overall value for option buyers. However, the current spot price (around $67,400) is at a discount of nearly 12% to the maximum pain point ($76,000). This significant deviation reveals two core logics:

First, before the crisis erupted, the market was in an extremely optimistic bullish sentiment, with substantial funds betting on breaking through the all-time high (the $75,000–$80,000 range) by the end of March, which directly pushed the maximum pain point higher.

Second, the outbreak of the geopolitical crisis constituted a strong external shock, suppressing the upward momentum of the spot price. But judging from the total open interest of 167,072 BTC (notional value exceeding $11.2 billion), long positions did not experience large-scale unwinding and stampede due to the war news.

Data shows that the current put/call ratio (based on OI) is 0.75. This value, being below 1, indicates that from a global存量 perspective, call option (Call) open interest still dominates absolutely. Particularly at strike prices of $75,000, $80,000, and even $100,000, there are massive call open interest piles (with single strike open interest reaching nearly 10k BTC).

However, it is worth noting that the 24-hour volume PCR (Put/Call Volume Ratio) reached 1.37. The divergence between存量偏多 (0.75) and增量偏空 (1.37) perfectly captures the current market psychology: long-term institutions maintain their original long exposure (not selling spot, not closing long Calls), but in the short term following the outbreak of the Middle East war, substantial funds rushed in to buy out-of-the-money put options (OTM Puts) for tactical hedging, leading to a surge in short-term Put trading volume.

Combining detailed option data from Deribit, we observe that the distribution of Delta values is extremely dense in the $67,000 to $70,000 range. The current spot price of $67,495 is right in the "meat grinder" zone of the bull-bear struggle.

If the geopolitical situation further deteriorates, causing macro funds to withdraw en masse, and the spot price breaks below $65,000 (a strong support level), market makers, to hedge their short Put exposure, will be forced to sell in the spot or futures market, potentially triggering a wave of localized negative liquidity feedback, testing the psychological关口 of $60,000 downwards.

Conversely, if the Middle East situation enters a stalemate stage mediated by major powers after a brief violent conflict, and once the panic sentiment peaks and recedes, the rebound in the crypto market will be extremely fierce. Due to the massive accumulation of Call options in the $70,000 to $76,000 range above, once the spot price stabilizes and breaks through the $70,000 resistance level, market makers will be forced to buy spot to hedge their negative Gamma exposure. This classic "Gamma Squeeze" effect will propel the BTC price towards the maximum pain point of $76,000 at an unprecedented speed.

The aftershocks of the Middle East geopolitical tremor will continue to ferment. The subsequent actions of the US and Iran will determine the final destination of global safe-haven funds. In the foreseeable short term, BTC spot will experience violent whipsaws within a wide range of $62,000~$70,000. Leverage in the contract market will be反复清洗 during this process. Quantitative strategies should focus on "reducing leverage and capitalizing on volatility," suitable for constructing calendar spreads or grid market making at key support and resistance levels, avoiding unilateral trend exposure.

Judging from the option持仓结构, the massive expiration on March 27 is a gravitational center the market cannot bypass. Unless a global, uncontrollable World War III-level liquidity drought erupts, as panic sentiment marginally decreases, BTC's "safe-haven属性" and "anti-inflation属性" will be repriced. In mid-to-late March, the market is highly likely to initiate a restorative rebound, and the spot price has a strong incentive to move towards the $75,000–$76,000 range (the maximum pain point and dense Call strike zone).

This event marks the entry of geopolitics into a higher-risk phase. Whether it's the rekindling of inflation expectations brought by war (soaring crude oil) or the crisis of confidence in fiat currencies triggered by financial sanctions against specific countries, the strategic value of Bitcoin as a "borderless, non-sovereign hard asset" is being reinforced at the underlying logic level. For large institutions such as family offices and macro hedge funds, the单一的美元债+美股的60/40 portfolio can no longer cope with current tail risks. The allocation proportion of BTC as an "uncorrelated asset" in investment portfolios will undergo a systematic leap following this crisis.

The US and Israeli strike on Iran is the first thunderclap reshaping the global financial landscape in early 2026. Beneath the surface of panic, crypto option data冷静地揭示了机构资金's底牌 of "short-term defensive hedging, long-term依然看涨".

For professional financial practitioners, stripping away emotional noise and closely monitoring the trend of implied volatility changes and the transfer of market makers' Gamma exposure are the core codes to穿透战争迷雾 and grasp the next round of asset pricing power. With the $76,000 option maximum pain point standing like a lighthouse, every deep pullback caused by panic is accumulating potential energy for the future breakthrough.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush